(Illustration by Mark Allen Miller)

(Illustration by Mark Allen Miller)

The Bill & Melinda Gates Foundation, the world’s largest family foundation, is also one of the world’s largest impact investors. Since 2009, the foundation has complemented its grants budget with a substantial allocation for program-related investments (PRIs). In the words of Julie Sunderland, the founding director of Program Related Investments: “While the majority of the foundation’s activities will still be traditional grantmaking, we believe PRIs can be a critical tool to stimulate private-sector innovation, encourage market-driven efficiencies, and attract external capital to support our charitable priorities.”1

Making Markets Work for the Poor

This special supplement examines how the Bill & Melinda Gates Foundation uses program-related investments—loans, equity stakes, and guarantees—to complement its traditional grant making.

-

Philanthropy’s New Tools for Innovation and Impact

-

Leveraging the Balance Sheet

-

Neglected No More

-

Unintended Consequences

-

Banking on the Poor

-

Guaranteed Impact

-

Investing for Impact with Program-Related Investments

-

Tough Love

-

Eyes Wide Open

-

Returns on Investment

-

Private Financing for Public Education

A PRI (as described more fully below) is a loan, equity investment, or guaranty, made by a foundation in pursuit of its charitable mission rather than to generate income. The recipient can be a nonprofit organization or a for-profit business enterprise. The US Internal Revenue Code treats PRIs similarly to grants. In contrast to ordinary investments from their endowments, foundations do not expect PRIs to produce market-rate returns.

Today, the Gates Foundation has allocated $1.5 billion to fund PRIs, of which it has committed $1 billion across 47 investments. Its PRIs have allowed the foundation to reach beyond the nonprofit sector to draw on the talent, expertise, and innovations offered by the private sector to advance its mission to “help all people lead healthy, productive lives.”

With its PRIs, the Gates Foundation has invested to scale up enterprises that serve the poor. It has guaranteed public agencies’ purchase of vaccines and contraceptive implants in order to convince large pharmaceutical manufacturers to boost their production and reduce prices for the benefit of those most in need. And it has made equity investments in biotech startups to induce them to focus on neglected diseases such as malaria and tuberculosis.

For example, the Gates Foundation made a PRI in M-KOPA, a Nairobi-based for-profit startup that sells solar lighting and mobile phone charging systems on a pay-as-you-go basis to East African households. To establish asset-backed lending to the poor as a bankable proposition, the foundation made a loan secured by receivables from the company’s customers, who pay for their solar products over time. This 2013 loan was made in partnership with a local commercial bank, allowing M-KOPA to develop a credit history that would attract future commercial lenders. The foundation’s loan was accompanied by a grant to support new product development and expansion into new geographic areas. (See the article “Banking on the Poor” for more details on the foundation’s investment in M-KOPA.)

The Gates Foundation has also made PRIs in biotech start-ups as part of its commitment to the development of new vaccines, therapeutics, and diagnostics for infectious diseases that disproportionately affect individuals living in developing countries. Some of the most promising research and new product development in biotech emerges from technology platforms in early-stage, venture capital-backed companies. However, biotech firms understandably face pressure to focus on commercially attractive markets. The Gates Foundation has coupled its equity investments in some of these young companies with “Global Access” side agreements that require the companies to make their products affordable in low-income countries. In some instances, the foundation has supplemented the investments with grants to fund the research and development of particular high-priority products. (See the article “Neglected No More” for more details on the foundation’s biotech investments.)

The accompanying case studies document the failures as well as successes of these and others of the foundation’s PRIs. This essay uses the example of the Gates Foundation’s grants and investments to support bKash, a mobile money service in Bangladesh, to illuminate critical elements of the foundation’s PRI strategies.2

Building on global advances in mobile communications and digital payment systems, the Gates Foundation seeks to provide affordable and reliable financial tools for digital cash transfers and savings. Poor people in Bangladesh face significant barriers to accessing financial services. Because their transactions are mainly cash-based, they confront high risks and costs in storing, sending, and receiving money. Moreover, their limited access to financial services increases the costs for formal institutions, such as governments and companies, to transact with the poor, disincentivizing them to do so.

Beginning in 2009, the foundation’s Financial Services for the Poor program supported bKash through a series of grants and a PRI to enable it to build and operate a mobile payment platform in Bangladesh that would reach the poor, including the many residents of rural areas who subsist on less than $2 a day.

PRIs in companies such as M-KOPA, the biotech firms, and bKash are particularly useful where, without some external stimulus, private markets fail to meet the needs of the world’s poorest inhabitants for essential goods or services. The Gates Foundation’s website explains its approach: “In the case of business, we work with companies that have experience creating and delivering innovations that can benefit people living in poverty. These businesses bring tools, knowledge, influence, and money to the table. But they don’t always have an incentive to focus on inequities or to make sure their innovations reach everyone who needs them. When opportunities arise—when there is a chance to involve businesses that would not otherwise participate—we seek to create those incentives and encourage businesses to take action that does the most good for the most people.”3

Video: The Stanford Center on Philanthropy and Civil Society hosts a discussion motivated by this article and others in the series.

A Real-Time Experiment

For most PRIs, the [Gates] foundation has deep expertise in the neglected disease, cause of poverty, or educational challenge that the company is working to overcome.

PRIs are not typical investments. The Gates Foundation’s PRIs, designed to accomplish the foundation’s charitable mission, are driven by program teams that include some of the world’s top experts in global health, global development, and education. Its depth of in-house knowledge gives the foundation a unique perspective on how market-based solutions can serve its beneficiaries’ needs. The program teams work in tandem with a team of investment experts and lawyers to negotiate term sheets and agreements, address the legal complexities involved in PRIs, and support the investments post-close.

The Gates Foundation’s influence—a combination of its mission, money, reputation, and willingness to take considered risks— allows it to negotiate especially favorable terms for the benefit of the poor. Its Global Access agreements with pharmaceutical companies and other investee partners, for example, provide preferential pricing for the foundation’s target beneficiaries. The foundation also reserves the right to withdraw its investment if the agreed-upon charitable purposes are not being fulfilled.

The Gates Foundation is treating its PRI process as a real-time experiment. Its hypothesis is that leveraging resources through collaboration with private investors and for-profit entrepreneurs can drive high impact. “We’ve been doing this for a few years and are starting to draw a few conclusions,” Sunderland says. “But we still have a lot to learn.”

Even at this early juncture, however, the Gates Foundation’s experience and practices provide valuable lessons for other foundations considering their own approaches to PRIs, and for other strategic social investors seeking to use financial instruments to generate charitable benefits.

Investing For Impact

For a foundation, “impact” means achieving outcomes that would not otherwise have occurred in the areas of its concerns. Such additionality4 is a norm for the Gates Foundation, which has two fundamental criteria for every potential grant or PRI: Are we achieving the program’s charitable goals? Would this happen without us?5

For an organization funded by a foundation to have impact means not just that a program team’s intended outcome has occurred (for example, fewer instances of malaria), but that the organization’s activities contributed to that outcome (for example, the reduction in the disease was the result of a vaccine supported by the foundation and not of an especially cold summer).6 By the same token, for a foundation’s own investment to have impact, it must provide capital that an organization would not otherwise have, thus contributing to an increase in its charitable goods or services (such as vaccine doses); or it must induce the organization to provide goods or services at prices affordable by those in need that it would not otherwise have produced and distributed.

Grants are by far the main form of foundation funding of nonprofits. Aside from some PRIs in the form of low-interest loans and guaranties (to help purchase a building, for example), nonprofits have not been the recipients of investments, and certainly not of equity investments, because they cannot have owners.

In contrast, the typical recipients of the Gates Foundation’s PRIs are for-profit enterprises that strive to make a profit for their owners. When a foundation’s charitable objectives are served by for-profit organizations, it can further those objectives through a grant, contract, equity investment, loan, or guaranty.

The concept of PRIs originated in the US Tax Reform Act of 1969. Since then, foundations, including Ford, Rockefeller, MacArthur, and Packard, have used PRIs creatively to further their charitable missions. The Gates Foundation began its PRI program as a $400 million pilot in 2009 and has dramatically expanded the use of the tool. Its current $1.5 billion allocation is the largest commitment to PRIs in the world.

PRIs are conceptually and legally distinct from two other kinds of socially-minded investments that foundations can make: mission- related investments (MRIs) and socially responsible investments (SRIs). MRIs typically are investments in publicly-traded companies whose activities are aligned with a foundation’s charitable mission.7 SRIs are investments in companies that, whether or not so aligned, adhere to good environmental, social, and corporate governance (ESG) practices.8

MRIs and SRIs are part of a foundation’s ordinary portfolio of endowment assets and typically target risk-adjusted returns in line with those of traditional investments (so called “market-rate returns”). They are fundamentally different from PRIs, which do not have these financial objectives, but instead are designed to implement a foundation’s programmatic strategies.

The US Internal Revenue Code defines PRIs as investments that meet three criteria: the primary purpose is to accomplish one or more of the foundation’s exempt purposes; influencing legislation or taking part in political campaigns on behalf of candidates is not a purpose; and production of income or appreciation of property is not a significant purpose.9

The characterization of an investment as a PRI has four important consequences for a foundation.

- PRIs count toward a foundation’s qualifying distributions—the required annual payout of 5 percent of its endowment. (Any principal returned from a PRI must be regranted within a year; any income is treated in the same manner as income from regular investments.)

- PRIs are exempt from the US Internal Revenue Code’s penalty on foundations’ making “jeopardizing investments”—investments that, if only intended to increase a foundation’s balance sheet, would reflect a lack of reasonable business care and prudence (the “prudent investor standard”) in providing for the long- and short-term financial needs of the foundation for it to carry out its exempt function.

- PRIs (as well as grants) to for-profit organizations are accompanied by requirements of “expenditure responsibility” in monitoring the organization’s use of the funds—requirements that are not imposed on grants to public charities.

- A PRI commitment must “specify the purpose of the investment and must include an agreement by the organization…to use all the funds received from the private foundation…only for the [charitable] purposes of the investment and to repay any portion not used for such purposes.”10 The US Treasury regulations require a charitable investor to be repaid its funding by an enterprise that abandons its charitable activity.

As long as a foundation complies with the Treasury regulations, it is free to adopt its own procedures for making PRIs. The procedures designed and adopted by the Gates Foundation ensure that every one of its PRIs has the potential to improve the lives of its intended beneficiaries and that the foundation’s funds are used solely for charitable purposes.

Making a PRI

Private foundations making PRIs face several major internal organizational questions centering on initiating the investments, conducting due diligence on their charitable and financial prospects, and monitoring and supporting the investments after they are made. In some foundations, these matters lie mainly outside the grantmaking programs and are handled by a separate investment team. In others, a program team is primarily responsible for the entire investment process, in consultation with investment professionals or intermediaries. Lawyers play an important role in both cases, drafting agreements and ensuring compliance with US Treasury regulations, securities laws, and other legal standards.

PRIs at the Gates Foundation are handled collaboratively by two separate teams. A program team, composed of subject-matter experts, typically initiates the PRI, as it would a grant, and is responsible for specifying the conditions of the investment necessary to achieve the program’s charitable goals, as well as monitoring and evaluating charitable impact. A PRI team, with expertise in private equity and venture capital, structures the transaction and evaluates its financial risk. The PRI team brings to bear many of the same analytic skills and tools that a commercial investor would.

The process begins with a program officer who is responsible for grantmaking in the subject area of the PRI. In the case of the Gates Foundation’s investment in the Bangladesh mobile payment company bKash, Lynn Eisenhart, a senior program officer in the Financial Services for the Poor program of the Global Development Division, reviewed the potential investment just as she would have reviewed a potential grant. After deciding to go forward, the program officer then seeks co-sponsorship of the PRI with an investment expert from the foundation’s PRI team.

Assuming support from the PRI team, the next level of programmatic review is done by the Gates Foundation’s nine-person PRI Investment Committee. The committee includes representatives from program teams across the foundation as well as the chief financial officer and the general counsel. This group is responsible for reviewing each proposed deal to ensure that its potential for charitable impact justifies the investment risk as well as the significant burden that each investment places on foundation resources. On the basis of its assessment of charitable impact and investment risk, the committee makes a recommendation, which incorporates diverse technical and charitable perspectives and ensures that the scarce resources of the PRI and legal teams focus on the highest-impact opportunities.

If the committee recommends pursuing the deal, the investment is reviewed by the president of the applicable division (Global Development, in the case of bKash). If the president is confident that the investment will further the division’s charitable goals, it is recommended for ultimate approval either by the foundation CEO or, if it exceeds a certain threshold, by the foundation’s co-chairs, Bill and Melinda Gates. The multi-stage review process leading to a PRI at the Gates Foundation is aided by several critical tools and concepts, described in the sections that follow.

Ensuring Charitable Impact

The Gates Foundation has systematized several practices that tend to ensure or amplify the direct charitable impact of the PRI:

- Global Access | Requiring that knowledge and information generated by foundation-funded projects will be promptly and broadly disseminated, and that the funded developments (such as pharmaceuticals) will be made available and accessible at an affordable price to people most in need.11

- Licensing Rights | Requiring that in the event the PRI recipient fails to adhere to its Global Access or other charitable commitments, the foundation would obtain the intellectual property rights necessary to take the project forward with another partner.

- Building the Field | Ensuring that critical lessons learned by the PRI recipient and the foundation are shared with the broader research, educational, philanthropic, and business communities.

The Concept of Risk Share

Unlike some impact investors who demand competitive rate-of-return along with social impact, the Gates Foundation never makes PRIs for the purpose of achieving financial returns. The foundation invests even though it is likely to lose capital. This approach is consistent with the concept of additionality as well as conditions for PRIs under the tax code.

The foundation is realistic about the types of often high-risk and low-return investments that it makes on behalf of its beneficiaries. Overall, the foundation anticipates approximately a 10 percent loss on its PRI capital. In other words, for each dollar invested, 90 cents will ultimately be returned. (Of course, for a grant the “loss” is 100 percent, because none of the money is returned to the foundation.)

Unlike some impact investors who demand competitive rate-of-return along with social impact, the Gates Foundation never makes PRIs for the purpose of achieving financial returns.

The Gates Foundation takes specific steps to quantify the expected loss on each investment. The process (described in detail later in the essay) applies a financial analysis to the PRI to determine the investment’s “Risk Share.”

Estimating the expected loss from the foundation’s investment gives the foundation an internal mechanism for allocating the total investment amount between the PRI budget and the relevant program budget. Typically, the Gates Foundation requires that an amount equal to the expected loss be paid out of the program team’s grant budget as its Risk Share. Requiring the program to have “skin in the game” provides further assurance of the PRI’s charitable impact and considered use of the foundation’s resources.

Pricing the Risk Share gives the foundation flexibility to undertake a variety of types of investments that individually may have expected losses ranging from 100 percent (such as equity to support a very early-stage, high-risk technology in an uncertain market) to as little as 1 percent (for example, guaranties that result in tens of millions of dollars in savings for global health funders but have low likelihood of being called).

The Risk Share has enabled the Gates Foundation to fashion PRIs to achieve particular charitable objectives. It frees the portfolio from general mandates such as “capital preservation,” which could result in a homogeneous collection of, say, low-risk loans. And sharing the financial risk ensures that a program team is appropriately engaged to pursue and assess the charitable impact.

Evaluating a PRI’s Charitability

One of the required characteristics of a PRI is that “no significant purpose of the investment is the production of income or the appreciation of property.”12 The IRS has provided limited guidance as to what this means in a regulation that states: “In determining whether a significant purpose of an investment is the production of income or the appreciation of property, it is relevant whether investors who engage in investments only for profit would be likely to make the investment on the same terms as the private foundation.”13

Unfortunately, this does not offer a clear standard. Rather, it leaves private foundations struggling to find a balance between investing on such unfavorable terms as to result in an impermissible private benefit to the company or other shareholders, and investing on terms that are so favorable that financial return appears to be a significant purpose of the investment.

Given this delicate balance, the Gates Foundation obtains a legal opinion from a tax attorney experienced in private foundation law in connection with each PRI. The opinion, written by internal or external counsel, reviews the transaction, documents, and other pertinent information, states the facts, articulates the charitable purpose for supporting the PRI recipient with investment capital, identifies the critical terms documenting the PRI recipient’s commitment to the charitable purpose, and concludes with a reasoned discussion of how these facts align with regulations governing private foundations.14 The legal opinion also provides a vehicle for ensuring the proportionality of the foundation’s investment against the extent of the recipient’s charitable commitments.

Modes of Funding: A Deeper Look at BKash

How does the Gates Foundation determine whether and how much to fund a potential partner, and whether to structure its support as a grant, a PRI, or some combination of these? bKash provides an excellent case study for considering these questions.

The origins of bKash can be traced to the Gates Foundation’s interest in promoting financial inclusion in Bangladesh, Bangladesh’s BRAC Bank’s mission to facilitate small and medium enterprises not served by conventional banks, and two Bangladeshi-American brothers’ interest in founding a mobile money company in that country.

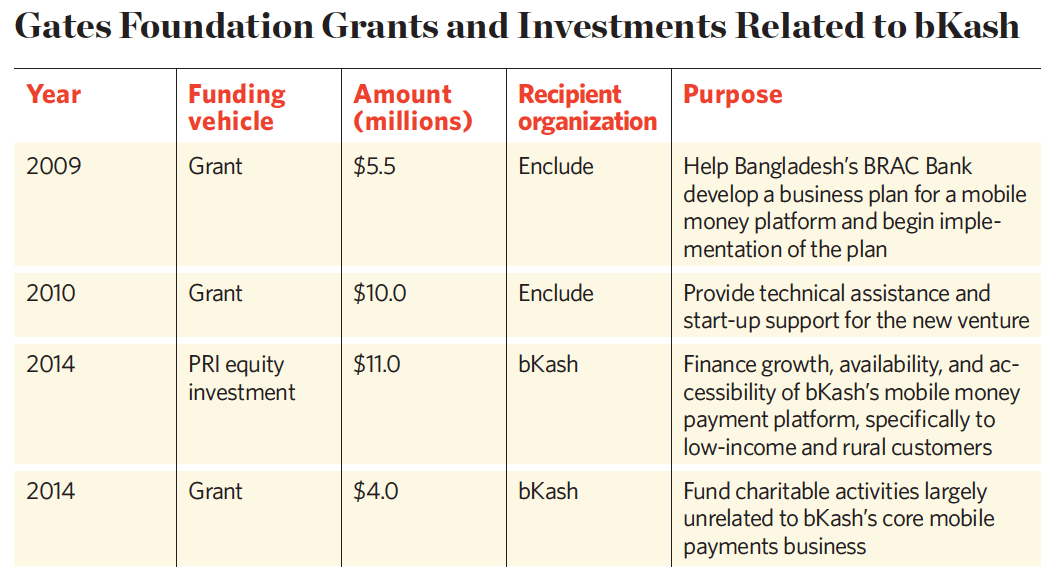

The Gates Foundation’s initial support came in the form of two grants from the Financial Services for the Poor (FSP) program team to the global consulting firm Enclude.15 A $5.5 million grant in 2009 enabled Enclude to assist BRAC Bank in developing a business plan for a mobile money platform. The foundation believed that such a platform would allow the bank to offer greater financial inclusion for the poor, but also understood that the venture would accumulate millions of dollars in operating losses before breaking even. BRAC Bank, which was required to own a majority of bKash for the latter to receive licensure, was unlikely to support a loss-making venture that would impair its legally prescribed capital reserve.16

At about the same time, Money in Motion LLC, a US investment firm led by telecom entrepreneurs Iqbal and Kamal Quadir, was also recognizing the potential for mobile money in Bangladesh. It sought a partnership with BRAC Bank to form a for-profit mobile payment company to be known as bKash—after bikash, the Bengali word for “growth.” In the first quarter of 2010, Money in Motion and BRAC Bank cemented an agreement, and bKash obtained a license to operate as a subsidiary of the bank.

In November 2010, the Gates Foundation’s FSP program team made a second grant to Enclude, this time $10 million, to support the growth of the newly formed bKash. It was hoped that if bKash could replicate the scale of other mobile payment platforms, most notably M-Pesa in Kenya, the company would accelerate cash digitization and financial inclusion for the benefit of the poor in Bangladesh.

By the end of July 2013, bKash was serving more than 4.2 million registered customers and had built a network of more than 60,000 mobile money agents, many of them assisting the poor and underserved in making use of the novel technology. It had become the market leader in Bangladesh.

The 2009 and 2010 grants to Enclude had been essential to get the venture started, but all of the parties involved recognized that bKash now needed actual investments. The company had recently closed a $10 million equity investment from the International Finance Corporation (IFC), and bKash’s management estimated that it needed an additional $15 million to fund its growth through the point of cash flow breakeven. With commercial capital scarce in Bangladesh, especially for firms focused on financial inclusion of the poor, bKash sought the Gates Foundation’s direct support.

When funding a nascent enterprise, the Gates Foundation seeks to achieve four fundamental goals:

- Further the charitable goals of the foundation’s program team.

- Assure that the capital structure of the business is healthy and matched to its ability to generate returns.

- Avoid distorting the financial market for goods or services in the sector in which the investment is made.

- Encourage good governance and exert an appropriate amount of influence over the recipient enterprise’s management.

For the Gates Foundation to achieve these goals when investing in a startup in a developing country almost always requires a subsidy, which is inherent in the type of support provided through grants and PRIs.

Because bKash was not ready to attract commercial investors, Gates Foundation staff had no doubt that it required a subsidy to thrive and grow. The question was how much. The underlying economic principle is self-evident: the total subsidy should be the amount of capital needed for the company to reach a market-sustainable level of risk-return that would attract commercial capital, and must be justified by the public good created by the subsidy. Less subsidy would, by hypothesis, compromise both the enterprise’s chances of success and the foundation’s related charitable goals. More subsidy would waste resources that could be devoted to other charitable purposes, create a risk of distorting the market, and possibly even confer an impermissible private benefit. Ultimately, application of the principle to particular cases is a subtle judgment that draws on the combined expertise of the program and PRI teams.

Grant, Investment, or Both?

In crafting its investment in bKash, the Gates Foundation’s staff first faced the question of what form its funding should take. Grant funding had been the appropriate vehicle when bKash was just starting. Its millions of dollars in operating losses would have deterred BRAC Bank from participating in the initiative. As Lynn Eisenhart, FSP’s senior program officer, said, bKash was “a startup organization with a little money, but a lot of promise.”

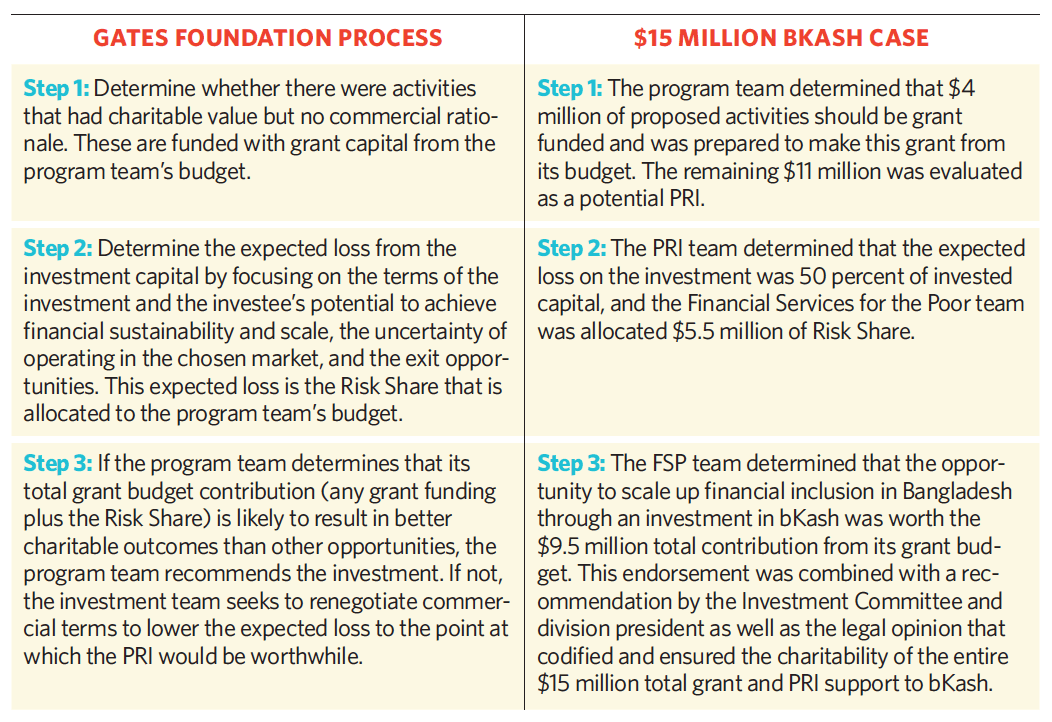

To determine whether any portion of the company $15 million need might appropriately be met through a grant, Eisenhart evaluated the use of the funds. Eisenhart identified $4 million of planned activities that provided significant charitable value to low-income people in Bangladesh but provided only marginal support for bKash’s mobile payments business. These activities included improvements in data collection, pilot programs with nonprofit partners, and exploring interoperability with other banks with the ultimate aim of broadening access for those most in need.

But it was also time for bKash to raise additional funds in a more conventional business-like manner in order to begin to demonstrate sustainability. The FSP team considered whether to make a PRI in bKash. Eisenhart and David Rossow, the senior program-related investment officer working on the deal, hoped that the investment would support bKash’s rapid growth in low-income and underserved areas and help attract commercial investors to the next round of funding to increase the likelihood of the company’s sustainability.

Eisenhart and Rossow realized that a loan of any amount would saddle the nascent enterprise with an obligation that could inhibit its growth and deter commercial investors. Moreover, a loan did not match the risk profile of an early-stage business with negative cash flow. They ultimately decided on a combination of an $11 million equity investment and a $4 million grant.

Besides sending a signal to commercial investors, a PRI may have other advantages over a grant. In general, a company’s management is more disciplined in meeting its obligations to an investor than a grantee is to a grantmaker. For example, the terms of the equity investment compelled bKash’s board to engage in a rigorous review of its governance, which would be unusual in most grant agreements. Indeed, a PRI may induce a foundation itself to be more disciplined in its funding. For example, the Risk Share negotiation between the Gates Foundation’s PRI team and a program team presses the staff to scrutinize every aspect of the enterprise, including country risks and the dynamics of the markets in which it operates.

Moreover, a foundation can negotiate rights that are typical for an investor but would be highly unusual in the context of a grant. Investments often come with the right to appoint board members or, as the Gates Foundation prefers, to have board observer status, and to approve certain major decisions by the investee (such as sale of the company). In addition, investments can broaden the foundation’s recourse—through put rights, consequential damages, make-whole requirements, and the like—and give the investor priority claims on assets such as intellectual property if the company abandons the charitable objectives or goes bankrupt. These are claims that a foundation could not ordinarily make when funding with a grant.

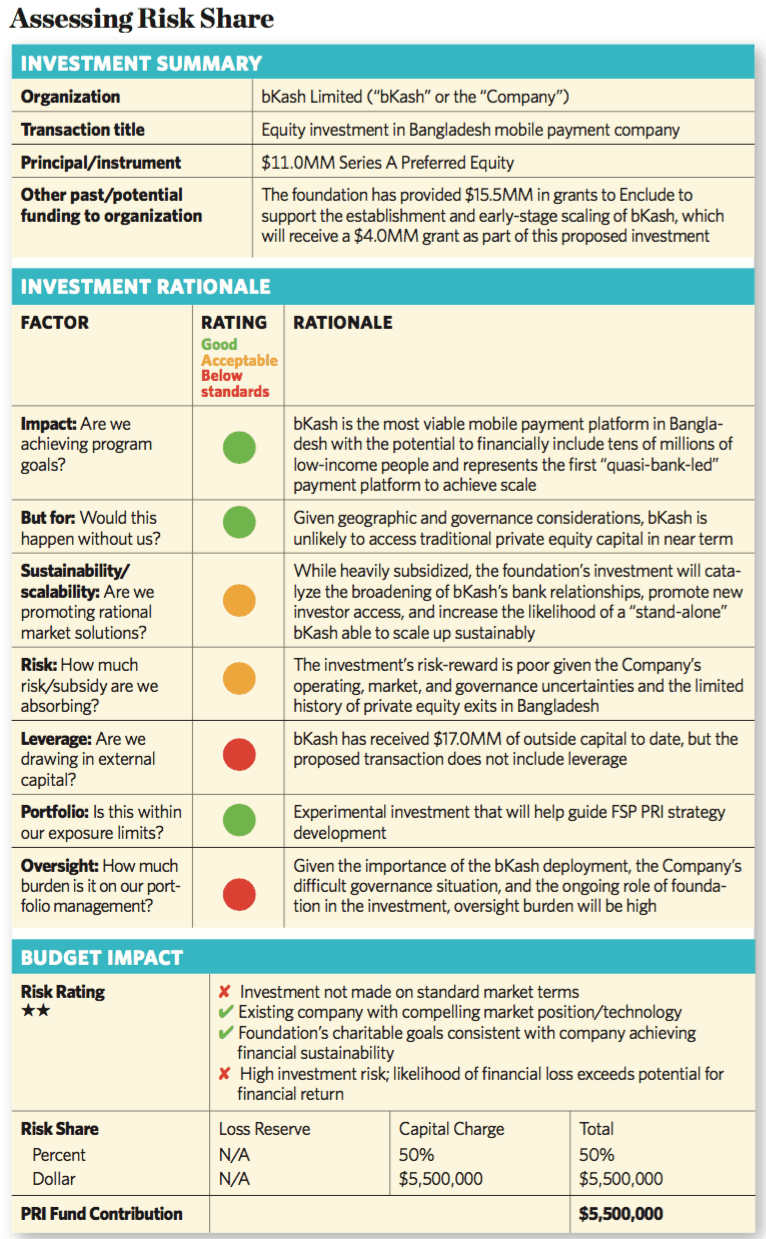

Assigning Risk Share in the BKash Investment

The Gates Foundation’s determination of how much risk to accept in each PRI begins with what it calls the “charitable investment thesis”— what the foundation hopes to accomplish with this partner through the PRI.

“The charitable objective of the investment lies at the heart of our analysis,” Sunderland explains. “By clearly defining program goals, we can differentiate the risks that make sense to accept from those that are likely to undermine our investment thesis.

“For example, it may make sense for the foundation to subsidize an unproven technology in order to test hypotheses that will inform future grantmaking and investments. If the program team’s goal is to scale up delivery of a low-cost product, the PRI team would evaluate early-stage technology risk through the lens of a traditional investor. If the risk can be mitigated, great. If not, the investment team would likely reject the investment unless it offered a truly fantastic potential charitable reward.”

The $4 million grant to bKash would come entirely out of the FSP program team’s budget. How much of the $11 million PRI was an expected loss that would be reflected internally in the Risk Share and also borne by the program team’s budget?

The Gates Foundation uses a robust method, involving present value and appropriate capital costs, to calculate expected loss. The PRI team’s analysis of the rationale for a particular investment and its risk is incorporated in a summary chart prepared for the foundation’s investment committee.

The charitable investment rationale for the investment in bKash was mixed. It was strong for impact because bKash was the most viable mobile payment platform in Bangladesh, with the potential to serve tens of millions of low-income people. It was also strong for additionality (“but for”) because the company was not yet able to raise ordinary private equity capital.

On the negative side, the investment lacked leverage because it was not tied to bringing in any additional capital. And the PRI team would have to devote considerable effort to oversight to help the investment achieve its programmatic objectives.

In the middle, the company had a fair chance of becoming financially sustainable, and it presented reasonable risks. The PRI team gave bKash a risk rating of two stars out of a possible four. Although the company had a strong market position and close alignment of charitable goals and financial return, the PRI team believed that the proposed investment lacked validation and company-building support from a traditional investor. All things considered, the foundation expected to lose fifty cents of every dollar invested in bKash and assigned the PRI a 50 percent Risk Share.

The high Risk Share also reflected traditional investment risk. These included the complicated nature of the regulatory environment and governance structure of a mobile money company in Bangladesh, uncertainties around a new business model in a new market, and the limited history of private equity exits in Bangladesh.

Typically these high risks would be offset by a low pre-money valuation, liquidation preference, and other “last-money-in” rights. But the IFC and other investors had set a relatively high valuation. The foundation focused its negotiation on obtaining commitments from bKash related to achieving charitable goals rather than pre-money valuation.

bKash’s potential as a financial inclusion platform for tens of millions of low-income people in Bangladesh led the FSP program to contribute both the $4 million grant and a $5.5 million Risk Share portion of the $11 million investment. In February 2014, the foundation closed its $11 million Series A Preferred equity investment in bKash.

Supporting Investees

Like a conventional venture capital or private equity investor, the Gates Foundation actively engages with a portfolio company to support its success. In addition, however, the foundation works to ensure the company’s effective use of the PRI funds to achieve their shared charitable goals. Where appropriate, the foundation provides an investee with technical assistance and helps identify and recruit needed talent for its board and senior management. Although foundation staff do not serve on an investee’s board of directors, they are often board observers.

One factor in the Gates Foundation’s decision whether to make a PRI is the ease or difficulty of supporting the investment, including the role that co-investors may play, for better or worse. The presence of other experienced investors with aligned interests is a significant plus. These investors can often provide the “company-building” support that the investments will require, thereby allowing the foundation to focus on helping the investee achieve its charitable objectives. The presence of investors with competing interests, or inexperienced investors who may not provide appropriate support to the company’s management, is a negative.

The first step in portfolio engagement is continuous monitoring. Monitoring a grant requires regular reports from and meetings with the grantee organization to check on progress and to make course corrections where necessary. A foundation making a PRI must also take special care to ensure that the enterprise is balancing its financial goals with the agreed charitable objectives.

In monitoring one of its loans to the nonprofit Root Capital, for example, a (reparable) breach of the terms of the agreement alerted the Gates Foundation to the organization’s weak financial systems. Because this posed a risk to both their shared charitable goals and the company’s financial viability, the foundation responded aggressively by imposing additional restrictions to induce the organization to improve its financial management capabilities. (See the article “Tough Love” for more details on the foundation’s investment in Root Capital.)

The Gates Foundation provides its investees the types of support pertinent to a particular investment tool. For loans, this may include creative thinking about future capitalization and refinancing strategies, as well as serving as a reference for other impact investors or more traditional capital sources. With investment funds, the foundation often participates actively on limited partner advisory boards and in helping investment managers remedy human capital deficits identified in the due diligence process. Guarantees like those for vaccines and contraceptives require deep coordinating support to ensure that the NGO worlds of procurement and delivery work effectively with the for-profit manufacturers. Support for equity investments has included recruiting management teams and boards of directors for seed-funded startups and, when necessary, working with other investors to replace underperforming CEOs.

The Gates Foundation takes its responsibility to support its investment portfolio seriously, even requiring that investment staff with burdensome portfolios of deals forgo new opportunities for a year or two until exits from existing investments free up their capacity. “We begin with the premise of ‘do no harm,’” Sunderland says. “Providing dilutive capital without then rolling up your sleeves to help build the company does harm. Add the fact that we are asking them to take on really tough problems, and bad impact investing has the potential to destroy good companies.”

The Gates Foundation’s portfolio engagement revolves around two sets of relationships—internally with technical experts in the relevant program area and externally with company management and other investors. For most PRIs, the foundation has deep expertise in the neglected disease, cause of poverty, or educational challenge that the company is working to overcome. Ensuring that its investee partners have access to the foundation’s own expertise sometimes is more valuable than its investment capital.

Accounting for a PRI

Unlike an ordinary investment, a PRI cannot have the primary purpose of realizing a profit. In making a PRI, a foundation expects returns below what a commercial investor would accept, including potential loss of capital. How should it be accounted for within a foundation?

To oversimplify a bit, a typical foundation classifies its funds in three ways:

- The foundation’s endowment or balance sheet, comprising cash and investments, and typically managed by internal professional investment staff or external managers.

- Its annual grants budget.

- Its annual administrative budget.

The grants and administrative budgets are generally funded out of the investment returns from the endowment or by drawing on the endowment itself.

A PRI is an investment that includes an expected loss. To understand how to account for this funding device, one needs to think about how a foundation manages its balance sheet.

Assume that the newly formed “Steady- State Foundation” wishes to maintain the value of its investable assets over time. Also assume that over the long run, Steady- State’s investment portfolio will return approximately 8 percent per annum and that inflation will be about 3 percent per annum. Under those assumptions, spending about 5 percent of its endowment annually (for both grants and administrative costs) will maintain the value of its assets in perpetuity.17

Now suppose that the SteadyState Foundation decides that instead of making only traditional investments, it will make a risky three-year, $3 million equity PRI. This hypothetical PRI has both a lower return than a comparable commercial investment and the expectation of some loss of principal. The gap between the expected amount returned on the PRI versus a portfolio investment is a subsidy from the SteadyState Foundation to the investee, which must be justified by the expected achievement of its charitable goals.

Given the lower return and higher likelihood of loss, the PRI clearly should not be treated as a portfolio investment, for any significant allocation of the SteadyState Foundation’s investment portfolio to PRIs would compromise its ability to maintain its charitable mission over the long term.18

If it doesn’t make sense to classify a PRI entirely as a portfolio investment, it makes no more sense to classify it purely as a grant: Unlike a grant, most PRIs don’t “cost” the full amount of the disbursed amount, because the foundation expects to recover at least some portion of the disbursement. For example, suppose that SteadyState Foundation makes a $10 million PRI loan in furtherance of its mission. Assume also that the loan is reasonably likely to get a 100 percent return of principal but carries a low interest rate, thereby sacrificing some interest income compared to a market-rate loan. Saddling the SteadyState Foundation’s program budget with $10 million of cost would unnecessarily and illogically foreclose other grantmaking from that same program’s budget.

The Gates Foundation solves this problem with the Risk Share, which allocates capital contributions for each PRI between two buckets: the balance sheet, managed through a revolving PRI fund with a maximum exposure of $1.5 billion at any one time, and the program team’s annual grant budget.

By blending its balance-sheet capital with the program team’s grants budget, the foundation is able to make PRIs with flexible levels of risk, thereby supporting entities with a variety of capital and investment needs. Requiring a Risk Share contribution from the program grants budget also ensures the program team’s accountability to the charitable objectives of the PRI by forcing the program team to make trade-offs between contributing to a PRI or using that funding for the alternative of grants.

To illustrate this process, let’s reconsider the $15 million funding request from bKash:

Results to Date

The performance of a PRI must be measured with both the tools used for ordinary financial investments and an assessment of the partner’s progress against the charitable purpose. The latter is far more complicated. Some charitable outcomes are hard to measure, and objectives and metrics can vary widely across investments. Quantifying the benefits of improving or saving lives through a malaria vaccine, for example, is radically different from assessing the success of a charter school or community college. For all practical purposes, these different goals are incommensurable, and any weightings placed on the outcomes are highly subjective.

The challenges of measurement become even more complex when success is defined not only by the outcomes of an individual enterprise, but by the dynamics of an entire industry or market. The Gates Foundation’s PRIs are often intended to tackle systemic market failures and to open the way for multiple market-based solutions that benefit those most in need.

Also, most of the Gates Foundation’s PRIs have long time horizons, and after only seven years it is premature to assess the success of its innovative program. Still, the foundation is beginning to see outcomes, especially for the shorter-term investments. Some of these are described more fully in the case studies that accompany this article.

Although the Bill & Melinda Gates Foundation is a relative newcomer to PRIs, the thoughtfulness of its processes and the breadth and enormous scale of its investments make its work groundbreaking. What lessons does the Gates Foundation’s experience with PRIs provide for foundations and other philanthropists who are using investments as tools to achieve social aims?

- Investing for impact is hard. | Any foundation can make PRIs, but achieving real charitable impact is difficult. As in grantmaking, the riskiest investments often have the greatest potential for impact but also the greatest likelihood of failure. High-impact PRIs are not for the faint-hearted. PRIs are inevitably more complex than grants because they balance two objectives—programmatic and financial viability— and require more due diligence, legal documentation, and engagement with a foundation’s partners. In addition to needing staff with investment expertise, PRIs demand vastly more legal and compliance work than most grants and require building deep relationships with investment partners to manage the inevitable challenges of their dual, and sometimes competing, objectives.

- Program and investment teams must work together. | The subject-matter expertise and skills of program officers are fundamentally different from those of investment professionals. It may be possible to recruit or train staff with cross-cutting expertise, but this is a practical impossibility in scientific and technical areas of rarefied knowledge. A glance at the biographies of members of the Gates Foundation’s Global Health team indicates that it would be difficult to recruit MDs and PhDs with their specialized experience who are also investment experts. The Gates Foundation’s PRI process is noteworthy in the close collaboration of members of the program and investment teams.

- Financial subsidies are both essential to PRIs and potentially hazardous. | PRIs include some expectations of loss—subsidies— which are counterbalanced by the investments’ ability to further a foundation’s charitable mission. Although subsidies can be crucial in launching new enterprises and new sectors, a funder must be vigilant not to distort markets or encourage entrepreneurial complacency.19

- Program staff should have skin in the game. | Every foundation aims to hold program staff accountable for their funding decisions. Allocating PRI-contributed capital between the Gates Foundation’s $1.5 billion PRI allocation and the program team’s budget through the Risk Share is an ingenious way to press the program team to justify the charitable value that the foundation is getting for its PRI dollars. Although every grantmaking foundation does this implicitly, the Gates Foundation’s processes demand explicit attention to the trade-offs.

PRIs are particular kinds of market-based approaches to solving the world’s social problems. As these approaches have gained attention in recent years, they have sometimes given rise to extravagant claims about “the end of philanthropy as we know it.”20 But rather than treating PRIs as an alternative to philanthropy, the Gates Foundation treats them as a valuable complement in situations in which markets can help achieve the foundation’s ambitious charitable goals.

Support SSIR’s coverage of cross-sector solutions to global challenges.

Help us further the reach of innovative ideas. Donate today.

Read more stories by Paul Brest.